Who Surveys the Surveyors?

Who invests in property?

And of those, who has ever had a surveyor make an absolutely ridiculous valuation on the property?

Hmmm, that’ll be every property investor then!

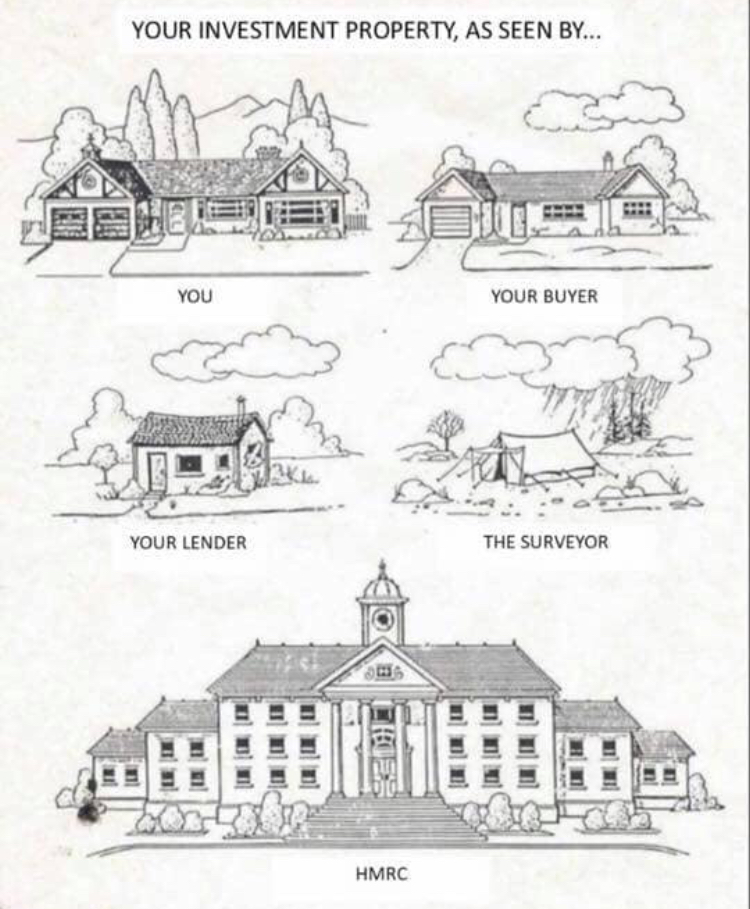

Despite our best due diligence, our most recent sold and for sale comparables, our best work, time and money spent in refurbishment… there will always be some utter clown of a surveyor who is more interested in covering their own arse than daring to admit what your newly-refurbished property is now actually worth.

What’s all that about?!

Sadly, it’s becoming more and more frequent to have a downvaluation: I’ve had it, my friends and all the local investors have had it, so it seems it’s a scourge across the board.

Surveyors obviously belong to some evil underground unit, where they get rewarded with downvaluation commission. There’s no logic to their madness.

What’s more infuriating is when the surveyors appear not to even look at the comparables, even when you give them them in their hand. And what’s doubly infuriating is that sometimes you are charged a surveying fee for them to go out and shaft you… #cry

One house I had last year was exactly the same as the comparable 4 DOORS DOWN, which had sold 7 months earlier. And although mine was newly refurbished, it was EXACTLY the same house, both with internal layout and outside grounds, but the surveyor still valued it lower than the twin one twenty metres away.

WHAT’S ALL THAT ABOUT?!?!

If I was if the murderous type, that surveyor would now be under the patio, Brookside style…

Still, what’s the point of my rant?

Well, to help you minimise the risk of this happening, and these are the things you can do to help that.

- Minimise the risk when you are doing your due diligence on the property by assuming the end value will be the worst-case scenario. Let’s be a pessimist here, then if some miracle happens and they do actually do their job properly, then anything above your worst-case prediction is a Brucie bonus. Good game, good game!

2. Look carefully at the comparable properties within a half mile radius in the last two years. And compare apples with apples, for instance a two-bed terrace is not going to be the same as a two bed semi-detached, so find houses that closely match what you have. Look at sold prices, and then current similar properties on the market.

3. Make a full list of every single refurbishments item you have done in the property. Don’t bother putting down what it cost you, it’s none of their business! Let them think you’ve paid more than the savvy tight-fisted bargain-hunting investor you are.

4. Take clear before and after refurbishment photographs during the project. The grimmer the better! (I mean grim before obviously!)

5. Meet the surveyor at the property, Even if it’s already tenanted, just explain to your tenant what is going on, and allay their fears that no, there is nothing to panic about, you’re not selling the house!

Be nice to the surveyor! Smile! Make genteel pleasant small talk, and point out things that were absolutely terrible in the house before you had your magic charm fixing them. Confirm the rental amount, with the tenancy agreement if required.

6. Prepare a little report pack, which you are happy to give to the surveyor. This should include details of the house, your list of refurbishment works, your before and after photos, and some Rightmove screenshots of comparable sold prices and current similar for sale values. Obviously, make sure you pick some examples which are in realistic keeping with your current property – it’s pointless showing them the other ones that sold really cheaply because they needed work!

7. Pray that your surveyor is not an absolute clown. Keep praying.

8. If the survey report comes back with a ridiculous valuation, you can either suck it up and take it, change lender (and thus surveyors), or get your mortgage broker to dispute it. If disputing it, work with your mortgage broker to build up a case of evidence, which politely shows, that actually, Mr Mortgage Surveyor, you’re talking tosh, and these are the reasons why.

9. Another option which may be considered, is to pay for your own independent RICS survey before the mortgage lenders surveyor goes out. This will obviously cost you a couple of hundred pounds, but it makes it more difficult for the surveyor to downvalue something, when you have placed in their hand a report from the Royal Institute of Chartered Surveyors.

10. Finally, if all else fails, seek out and destroy the surveyor. There is no other option.

Good luck, and let’s hope that the surveyors all get standardised and trained properly very soon!

# Disclaimer: no surveyors were harmed in the making of this blog or portfolio.

…but there’s always time…

When not entertaining herself with impromptu amateur photoshoots, Kellyann is a full time property investor and investment strategist, based in Leeds, West Yorkshire.

For further details of her work, and how she can help you, please visit:

{kind=link}